Business Credit Score NZ: What It Is, How It Works, and Why It Matters

A business credit score is one of the key components a lender looks at when assessing a funding application in New Zealand. Yet for many business owners, it is one of the least understood parts of the lending process.

At Bizzy, we see businesses apply for funding every day, and credit scores are one of the most common reasons a funding request is either not approved, or comes with higher interest rates than expected. In many cases, it's something that could have been addressed earlier.

This guide explains what a business credit score is, how lenders use it, and what Kiwi business owners can do to maintain and improve theirs before applying for funding:

What is a business credit score?

"Lenders use this score to assess the risk of lending to a business, a higher score generally improves access to credit and can lead to better terms."

– Monika Lacey, Chief Operating Officer at Centrix

What is a good business credit score in New Zealand?

While scoring scales differ across agencies, a general guide for NZ business credit scores is:

700 and above: Generally considered a strong score. Businesses in this range are more likely to access a wider range of lending options and may receive more competitive terms.

500 to 699: A moderate score. Most lenders will consider applications in this range, though terms may be less favourable

Below 500: This is considered the red zone, and a score in this range and can limit access to lending. Some lenders may decline applications in this range, while others may offer more restrictive conditions or require additional security.

While a core component, the credit score is not the only input into a lender decision. The business’ cashflow performance, revenue history, time in business and securities available are all important factors into how a lender assesses an application.

How is a business credit score calculated?

Credit scores are calculated slightly differently depending on the credit bureau, however they tend to all look at the same contributing factors including:

Company details & registration: Including basic registration information, trading history, and time in business.

Directors, Shareholders and Affiliations: This reflects how the business is owned, and tends to take into consideration whether directors and shareholders have experienced any credit issues

Credit defaults, judgements and tax defaults: This considers outstanding debts, overdue credit or unpaid tax obligations that are active.

Credit and repayment histories: This includes how reliably the business has met its repayment obligations over time or whether new credit applications or accounts have been opened recently.

How business and personal credit scores interact

Personal and business credit scores are separate, but they are not independent of each other. For SMEs, particularly those in the early stages of trading, a personal credit score can have a meaningful influence on how lenders assess a business funding application.

At Bizzy, we see lenders take a holistic view of both the business and the people running it. This is especially true for newer businesses where there is limited trading history to draw on. In the absence of established business credit data, lenders lean more heavily on the directors' personal financial track record to form a view of risk.

One of the considerations for a Credit Score could be how directors manage personal obligations, which extends to mortgage repayments, credit cards, and personal loans. While these transactions might not seem directly related to the business, they are treated as a meaningful signal of how the business owner, and therefore the business, is likely to manage business obligations like loan repayments.

If you are under sustained personal financial pressure, it is worth being aware that this can flow through to your business credit profile. It does not automatically affect your lending options, but it is a factor lenders will look at.

For business owners, particularly in the early years, maintaining a clean personal credit history is one of the most practical and often overlooked steps toward improving access to business lending.

How lenders use credit scores in lending decisions

A credit score is one of several factors a lender looks at when assessing a loan. Alongside the business and personal credit scores, lenders consider the purpose of the loan, available security, previous business financials, and future forecasts. The credit score matters, but it sits within a broader picture.

The credit score helps lenders predict future repayment behaviour based on historical financial conduct. A strong credit score can speed up the lending process, result in more competitive rates, and give lenders more flexibility on terms. A lower score may result in requests for additional documentation, more conservative loan amounts, or tighter conditions. It does not automatically result in a decline.

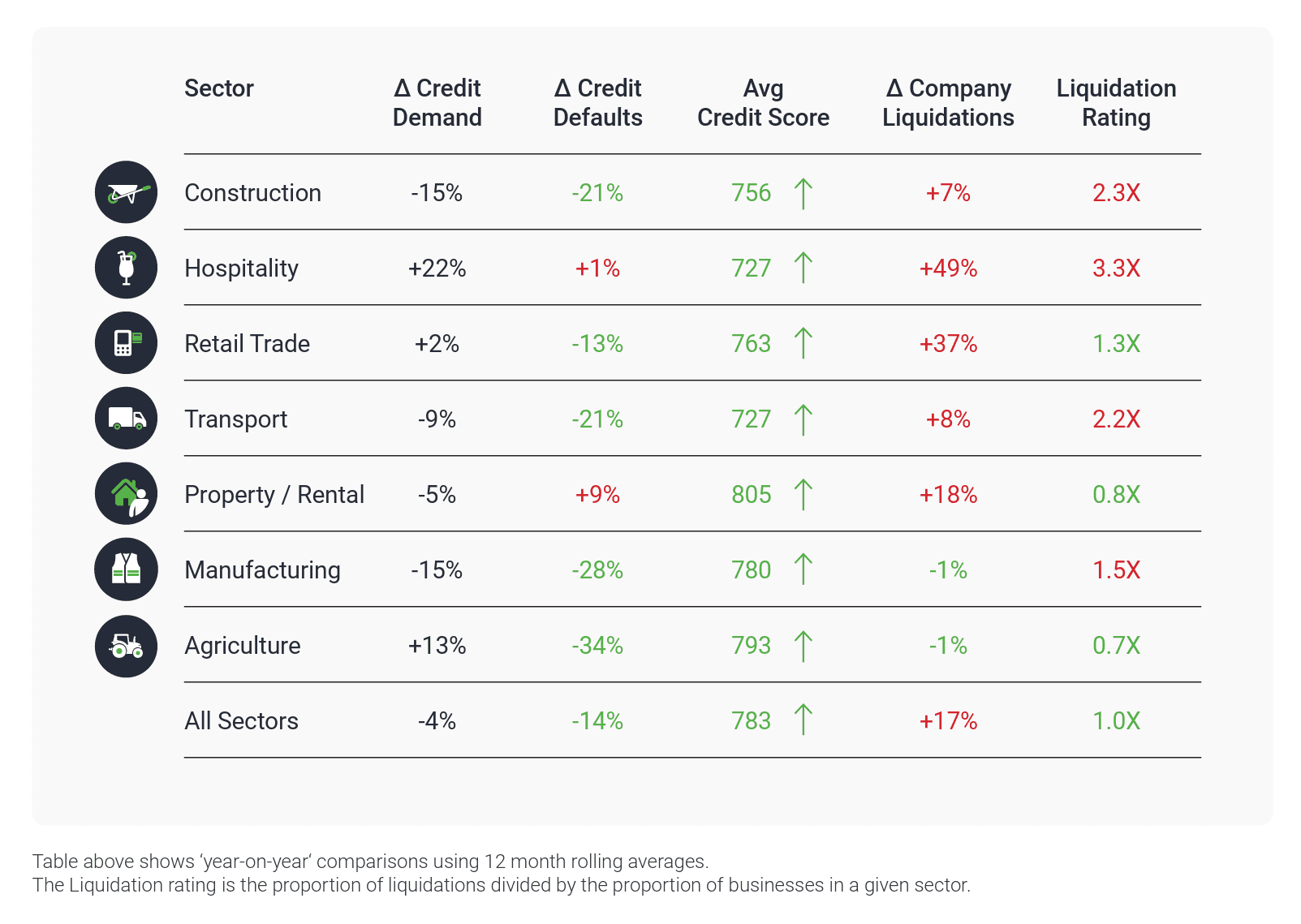

Sector context matters too. A credit score of 720 reads differently depending on the industry the business operates in. In a lower-risk sector, 720 can be a solid position. In hospitality or construction, where lenders are already applying tighter criteria due to currently elevated liquidation rates, the same score may carry more scrutiny. Lenders look at individual scores alongside sector averages to make a fully informed decision.

The table below shows the latest year-on-year sector comparisons from the Centrix May 2026 report.

Specialist lenders make up a significant part of the Bizzy lending panel and often take a broader view of creditworthiness than the main banks. They may place more weight on recent cashflow performance or the specific circumstances of a funding request, which can make them more accessible to businesses with lower credit scores or those operating in higher-risk sectors.

If you are planning to apply for funding in the coming months, understanding your current credit score and taking steps to improve it before you apply is one of the most practical things you can do to put yourself in the best position.

How to check your business credit score in NZ

You can request a copy of your personal credit report from the main credit reporting agencies in New Zealand, for example through Centrix.

Reviewing your personal credit report before you need funding is worth doing for two reasons. It lets you identify any inaccuracies and highlights how a lender might see you before they do. Doing this ahead of needing funding gives you time to address anything that could be improved ahead of lenders reviewing your application.

The main credit reporting agencies in NZ are: Centrix, Equifax and Experian

How to improve your business credit score in NZ

A business credit score is not fixed. There are practical steps you can take to maintain a healthy score over time, or to improve one that has slipped.

Pay on time. Payment history is one of the most visible signals on a credit file. Whether it’s loan repayments, supplier accounts, or tax installments - it’s important to pay these on time to reduce risk of missed payments or dishonours that will show up on your credit score. We recommend setting up automatic payments and having a sufficient balance in your accounts at all times to reduce the risk of failed payments due to non sufficient funds, rather than genuine financial difficulty.

Stay current with Inland Revenue obligations. Tax debt is reported to credit bureaus and treated seriously by most lenders. Since 2017, Inland Revenue has shared unpaid tax data with credit reporting agencies, meaning outstanding GST or provisional tax shows up on your business credit file. The Centrix April 2026 data confirms that IR activity continues to influence insolvency levels across NZ. If you are behind, addressing it proactively before applying for funding is important.

Limit credit applications. Every formal credit application generates an enquiry on your credit file. Multiple enquiries in a short window can signal financial pressure to lenders and lower your score. If you need to compare lending options, a platform like Bizzy allows you to receive indicative offers from 15+ lenders through a single application, with no hard credit checks run until you choose to proceed with a specific lender.

Check your credit file. Inaccurate information, such as a payment recorded as late when it was paid on time, or a settled debt that has not been updated, can affect your score unfairly. Reviewing your report before applying for funding allows you to identify and dispute any errors before a lender sees them.

Keep director and company information current. Ensuring your Companies Register details and director information are accurate as this is one of the key contributions to your business credit score - it’s a practical step that costs nothing.

Monitor your sector's credit health. Credit conditions vary significantly by industry. While construction and retail are showing early signs of improvement, hospitality remains vulnerable. Understanding where your sector sits helps you anticipate how lenders will approach your application.

What to avoid when it comes to your business credit score

Some of the most common credit score issues we see are avoidable with a little forward planning.

Missing or delaying payments. A single missed payment can remain on your credit file for up to five years. The impact is disproportionate to the oversight, which is why automated payments are worth setting up.

Falling behind on Inland Revenue obligations. Tax debt is one of the more consequential marks on a business credit file. It is reported to credit bureaus, flagged seriously by most lenders, and continues to influence insolvency levels across the NZ market. Set reminders in your calendar for key IR due dates to stay head.

Making multiple credit applications in a short period. Each separate application triggers a hard enquiry. This is one of the most common ways businesses could inadvertently lower their own score while actively trying to find the best lending terms. Instead of applying directly, use Bizzy to get multiple quotes before the lender does a hard-check.

Ignoring your credit file. Business owners who have never checked their credit report may be unaware of outdated or inaccurate information affecting their score. Take the time to review your credit score before submitting a significant funding application.

How applying with multiple lenders can lower your credit score

In New Zealand, not all credit checks are equal and it’s important to know the difference:

A soft check is an information-only enquiry which has no impact on your score.

A hard check is a formal enquiry which is recorded on your credit file that signals to lenders that you are seeking new debt

There is a hidden cost to shopping around for the best loan rate. Applying to three different lenders separately triggers three 'hard checks' on your credit file. This pattern, especially if the applications happen within a short period of time, can look like financial stress, which inadvertently lowers your score.

By trying to find the best loan offer for your business needs and applying with multiple providers, you may inadvertently lower your score, resulting in the very thing you were trying to avoid: a higher interest rate.

Usually, lenders are required to run a full credit report to assess a loan request, provide an offer and finalise funding. On Bizzy however, lenders are able to provide indicative quotes upfront, without doing a full application. They provide quotes based on key business information including 12 months bank transactions, profit and loss statements and the lending purpose. This means with one application through Bizzy you can reach 15+ specialist lenders across New Zealand and receive quotes without a hard credit check being run. The hard credit check only happens when you choose to proceed with a specific lender. With Bizzy, businesses can review indicative offers from multiple lenders side by side, compare rates and total costs, and make a decision with the full picture in front of them. All without the credit file impact of applying to each one separately.

Thinking about funding options for your business?

Bizzy lets businesses explore and compare lending offers from multiple lenders with a single application - helping you see the rates, fees, and overall costs in one place.

Frequently Asked Questions for Business Cashflow in NZ

Does checking my own credit score affect it?

No, checking your personal credit report is considered a "soft" enquiry and does not impact your score. Only formal credit applications will generate a "hard" enquiry against your credit score. You can order a personal credit report from any of the leading providers in NZ such as Centrix, Equifax or Experian.

What is a good business credit score in NZ?

Using the 0 to 1,000 scale, 700 and above is generally considered a strong score with access to competitive lending terms although can vary across sectors. 500 to 699 is moderate, and below 500 is considered high risk, which can limit lending options or result in a decline.

Will applying through Bizzy affect my credit score?

Not for the initial application. When you submit a request through Bizzy, your details are shared with lenders to generate indicative offers. This stage does not involve a hard credit check, so your score is not affected while you are comparing options. A hard credit check only happens when you choose to proceed with a specific lender and move from an indicative offer to a formal application.

How long do negative marks stay on a business credit file in NZ?

Most adverse credit information, such as late payments or defaults, remains on a credit file for up to two years. Court judgments and credit defaults may remain longer. Credit reporting agencies are required to remove information that is no longer accurate or relevant.

Can a new business build a credit score?

Yes, though it takes time. Opening a business bank account, maintaining supplier credit accounts in good standing, and meeting all financial obligations on time are the most practical starting points. For newer businesses, the directors' personal credit history carries more weight while the business credit history is being established.

What if a lender declines my application?

A decline from one lender or bank does not mean all lenders will decline. Different lenders have different risk appetites and assessment criteria. Specialist lenders often assess applications more holistically than the main banks. Bizzy's lending panel includes 15+ specialist lenders across a range of product types, and comparing options through a single application reduces the need to apply repeatedly, along with the credit impact that comes with it.

Does my personal credit score affect my business lending application?

For many NZ SMEs, particularly newer or smaller businesses, yes. Lenders regularly look at the personal credit history of directors alongside the business credit profile, particularly when the business does not yet have an extensive credit history of its own.

This article is for educational purposes only and provides general information about business credit scores in New Zealand. Bizzy does not offer loans, financial advice, or personalised recommendations. All finance options are subject to the individual lender's criteria and terms. You must assess any lender or offer yourself, and consult with a qualified financial adviser, accountant, or lawyer before making any financial decisions.